.webp)

The Top Climate Risk News Highlights For May

In the month of May, climate news centered around alarming rising temperatures and the impacts of climate change on various industries including oil and gas, insurance, and financial services. Learn more about how Jupiter is helping companies around the globe assess their physical climate risk, or request a demo.

#1. It’s looking like temps will be pushed into uncharted territory according to the WMO

According to a May 17 press release from the World Meteorological Organization, there is a 66% chance the annual near-surface global temperature between 2023 and 2027 will reach more than 1.5°C fuelled by heat-trapping greenhouse gasses and a naturally occurring El Niño event. And that there is a 98% likelihood that at least one of the next five years, and the five-year period as a whole, will be the warmest on record.

Secretary General Professor Taalas states that the next five years will push global temperatures into uncharted territory and will have far-reaching consequences related to health, food security, water management and the environment.

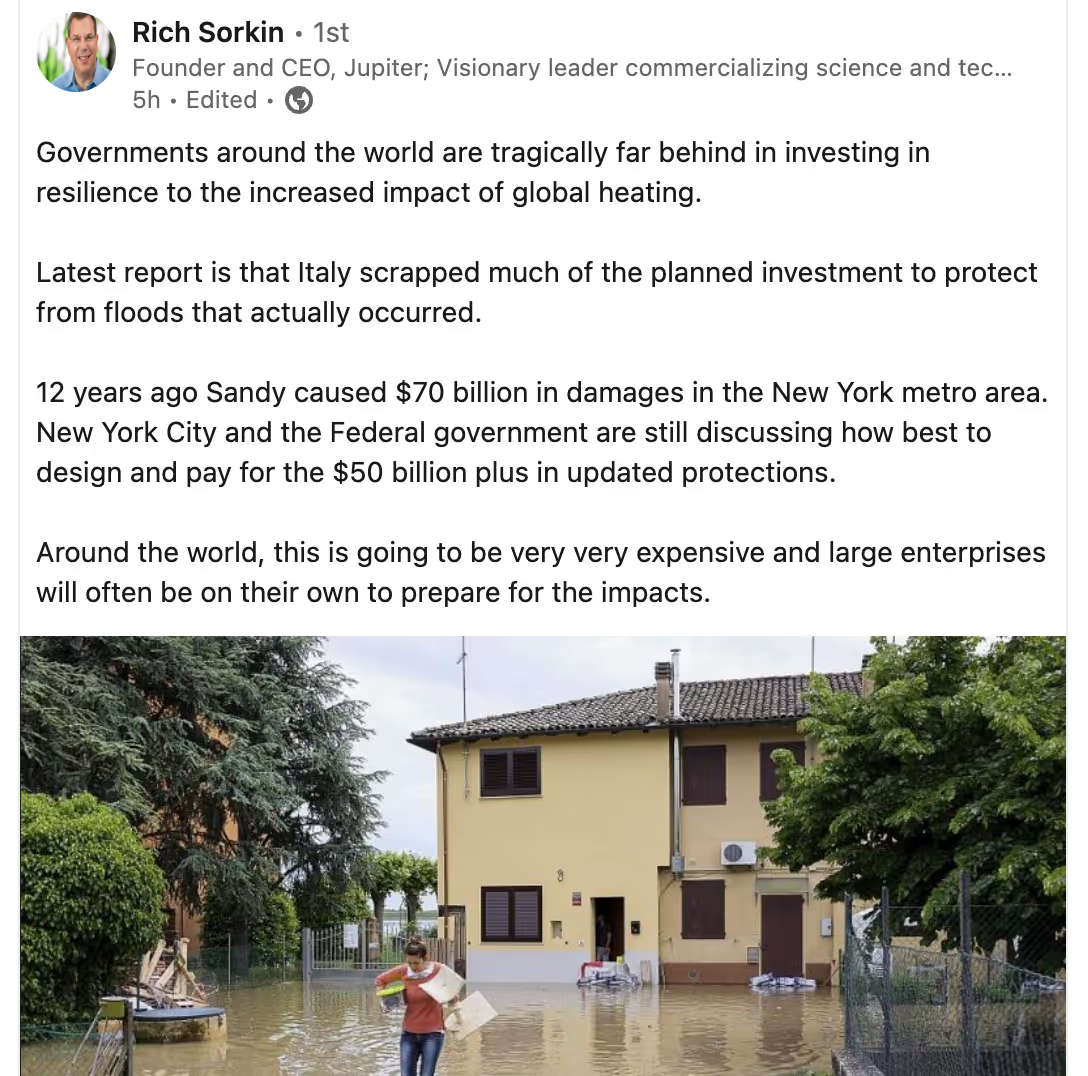

Jupiter’s CEO, Rich Sorkin, shared his perspective on his LinkedIn page just days ago calling on government agencies to get involved now and start investing to build resilience before it’s too late.

#2. A mortgage slump due to climate change?

The Environment Journal highlighted new research from Bain & Company that leveraged data from Jupiter ClimateScore Global that shows how major lenders are not adapting to reflect the growing risk of a climate-related mortgage slump.

The report reveals that only 18% of the world's largest banks have started incorporating physical risks to property in their mortgage lending strategies. The majority of these banks have neglected to include such risks in their strategy definitions, target frameworks, product ranges, and customer and client communications.

This is concerning considering the increasing threat posed by climate events, such as flooding, to properties worldwide. In several countries, a significant proportion of land is already at risk from these "physical perils," and this risk is expected to grow significantly in the near and medium-term. For example, the United States currently has 43% of its landmass considered at risk, which is projected to rise to 65% by 2050. Similarly, in Indonesia, 31% of land is at risk, and this figure is expected to reach 97% within the same period.

European countries also face similar challenges. Germany currently has 33% of its area under threat, which will increase to 68% in the next 30 years. Italy faces a similar situation, with 40% of its land at risk, projected to rise to 62%. A simulated bank model focused on Italy's portfolio suggests that without mitigation efforts, the value of mortgage collateral could drop by up to 15% by 2050, impacting profitability by as much as 10%.

Camille Goossens, senior partner at Bain & Company responsible for Sustainability and Responsibility Financial Services, emphasizes that climate change will profoundly impact properties globally, and no market is immune to its effects. However, many banks have not yet taken the necessary steps to adapt their business strategies and mitigate future climate-related risks. Without a comprehensive approach to addressing these risks in their portfolios, banks could face significant compromises in the future.

#3. The insurance industry is in need of more climate risk modeling

This month NPR covered the hot topic of extreme weather driven by climate change and how that is impacting the insurance industry. Climate-induced floods, hurricanes, wildfires and heat waves cause billions of dollars in damage every year in the United States alone. These growing costs are taking a toll on the insurance industry. Yet there’s hope that future-forward climate data and analytics will help insurers assess high-risk areas over the next 5, 10, 30 years, and adjust their business models to adapt.

What we’ve heard from insurance companies time and again is that there isn’t enough scientifically rigorous climate data available to accurately assess what the future looks like, and without this information, insurers aren’t able to build risk into underwriting.

This is where Jupiter comes in. We help insurers and lenders obtain an in-depth look at the risk across their entire portfolios to get a better understanding of what business processes will need to change to become more resilient to the impacts of a changing climate.

#4 Biden Administration Announced New Regulation to Limit Greenhouse Gas Pollution from Power Plants

On May 11, the Biden administration announced the first regulations to limit greenhouse pollution from existing power plants, which when combined with other climate policies in play, could greatly reduce the nation’s contribution to global warming.

It would set caps on pollution rates, which power plant operators would have to meet whether done through using different technologies or, in the case of gas plants, switching to fuel sources like green hydrogen.

The goal of the proposed regulations are to help eliminate carbon dioxide emissions from the nation's electricity sector. According to the New York Times article, the nation’s 3,400 coal- and gas-fired power plants currently generate about 25 percent of greenhouse gases produced by the United States, pollution that is dangerously heating the planet. The full New York Times article contains more of the details around the regulations.

********************************************************

Request a demo and we invite you to follow us on LinkedIn. For further information, please contact us at info@jupiterintel.com.