.webp)

Banking and lending

Inform capital strategy with defensible physical risk data.

Integrate physical risk into credit decisioning

Banks need more than historical loss data to understand how default patterns and collateral values shift under a warming climate. ClimateScore Global provides multi-hazard, asset-level metrics across 22.3 billion locations (22,000+ per site), with IPCC-aligned scenarios and flexible time steps extending to 2100.

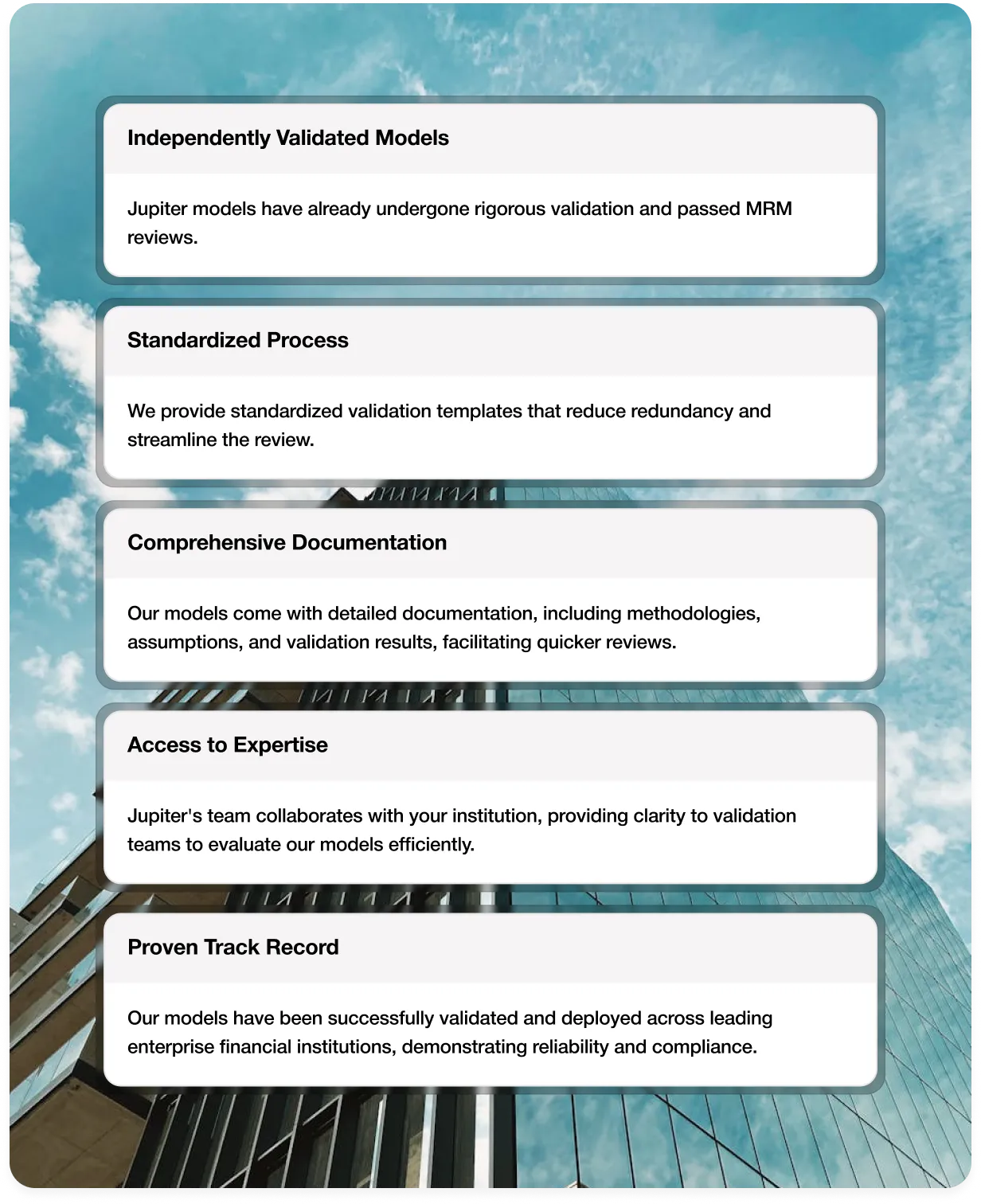

Accelerate model approval and reduce deployment delays

Jupiter has been validated by Tier 1 banks through their Model Risk Management (MRM) processes. With full documentation, co-developed validation tests, and deeply transparent methods, Jupiter’s models clear governance processes faster and with less friction.

Link hazard data to expected loss, market value, and capital impacts

Map climate exposure directly to the financial indicators banks rely on. Sensitivity analysis, expected-loss modeling, and scenario-driven stress tests bring clarity to how risk evolves across mortgages, commercial real estate, and corporate lending.

Improve capital planning and business continuity decisions

Banks use Jupiter to simulate extreme weather events, test operational resilience scenarios, and evaluate how acute events may influence liquidity, insurance costs, or borrower performance.

Identify concentrations, anticipate repricing, and act early

With asset-level modeling across global portfolios, banks can see where exposure concentrates, devaluation is likely, and opportunity lies.

The Jupiter Difference

ClimateScore Global is the only physical risk intelligence platform that combines trusted science, finance-grade outputs, full auditability, and real pathways to action.Its methods are transparent and peer-reviewed. Its metrics integrate seamlessly into financial models.

Documentation is built in. And every module — from RiskSignal to Adaptation Hub — helps you translate exposure into proactive capital strategy.