.webp)

.jpg)

Four structural changes in the 2026 GRESB cycle are quietly invalidating how thousands of real asset reporters have documented physical climate risk. Here's what shifted — and what it now costs to stay the same.

The Benchmark Has Moved

GRESB has positioned itself as the global standard for ESG performance in real assets over the past years. Now however, the 2026 cycle makes clear that they want this standard to carry real weight and become decision-useful for investors.

This year, the Foundation has moved decisively from rewarding participation to requiring performance. The physical climate risk questions in all five GRESB assessments — Infrastructure Asset, Infrastructure Fund, Infrastructure Development Asset, Real Estate, and Real Estate Lender — are now asking the same thing in sharper terms: not whether you have a policy, but whether you can prove what you did, at the asset level, in a way that a validator can verify.

That is a structural shift. And most 2025 responses won’t stand up under the new requirements.

Four Changes That Change Everything

The 2026 standard updates are concentrated in a handful of indicators, but their scoring implications are wider than the indicator count suggests. Four changes stand out.

The complete process or nothing. For Infrastructure Asset and Development Asset reporters, the four-stage environmental risk assessment — Identification, Analysis, Evaluation, and Treatment — is now binary. Complete all four stages for each material issue, with supporting evidence, or receive zero credit. Previously, partial processes earned partial credit. That option has been removed. The maximum scoring exposure across RM2.1, RM2.2, and RM2.3: -7.56 points.

If it isn't named, it isn't covered. Across all five assessments, evidence must specifically reference the reporting entity by name. A group-level policy that does not directly name the asset or portfolio will not satisfy the validation requirement. The maximum point exposure for sustainability reporting evidence that fails this test: -3.26 points.

CRREM's 2°C scenario is gone. The CRREM Foundation has discontinued its 2°C pathway, citing an inability to guarantee full scientific quality. For 2026 submissions across any assessment type, that scenario is no longer available. Firms relying on it need to migrate — now.

Coverage is now quantified. For performance indicators, scoring has shifted from a binary yes/no model to a sliding scale based on the percentage of the portfolio for which asset-specific evidence exists. Group-level frameworks that can't be traced to individual assets contribute nothing to your coverage percentage.

2025 was about showing you were engaged. 2026 is about proving what you did — at the asset level, documented, and defensible under scrutiny.

The Evidence Gap Most Reporters Don't Know They Have

The change that tends to create the most compliance exposure isn't the one that sounds the hardest.

Stage 3 of the RM2.1 requirement — Evaluation — is where most infrastructure reporters discover their evidence falls short. Identification and Analysis are increasingly well-executed. Treatment plans are directionally straightforward. But Evaluation requires something most generic risk assessments don't provide: a documented link between a specific physical hazard and its financial consequence for a specific asset.

Knowing that a facility faces elevated flood risk is not enough. The evaluation must connect that hazard to an estimated financial outcome — a damage figure, an insurance premium impact, a change to net operating income. Without that link, Stage 3 is incomplete. And an incomplete Stage 3 earns the same score as no assessment at all.

The same logic applies in different forms across all four of the 2026 changes. What's being tested in every case is whether your evidence is specific, financial, and named to the entity — or whether it's the kind of documentation that worked in 2025.

What Translating Hazard Risk to Financial Impacts Can Reveal

Consider a heavy fabrication and assembly facility in Hong Kong's Sham Shui Po district. Under today's circumstances, the flood water at the 100-year return period reaches over 0.6 meters at this location. By 2040, under the SSP5-8.5 scenario, that same return period produces close to 0.9 meters — a 36% increase in depth, driven by a combination of sea-level rise and intensifying storm systems. At the 20-year return period, the change is more acute: depth nearly triples, from 0.10 meters today to 0.30 meters by 2040.

Those are hazard metrics. What GRESB's 2026 standard — and any meaningful investment process — actually requires is what comes next: the financial translation.

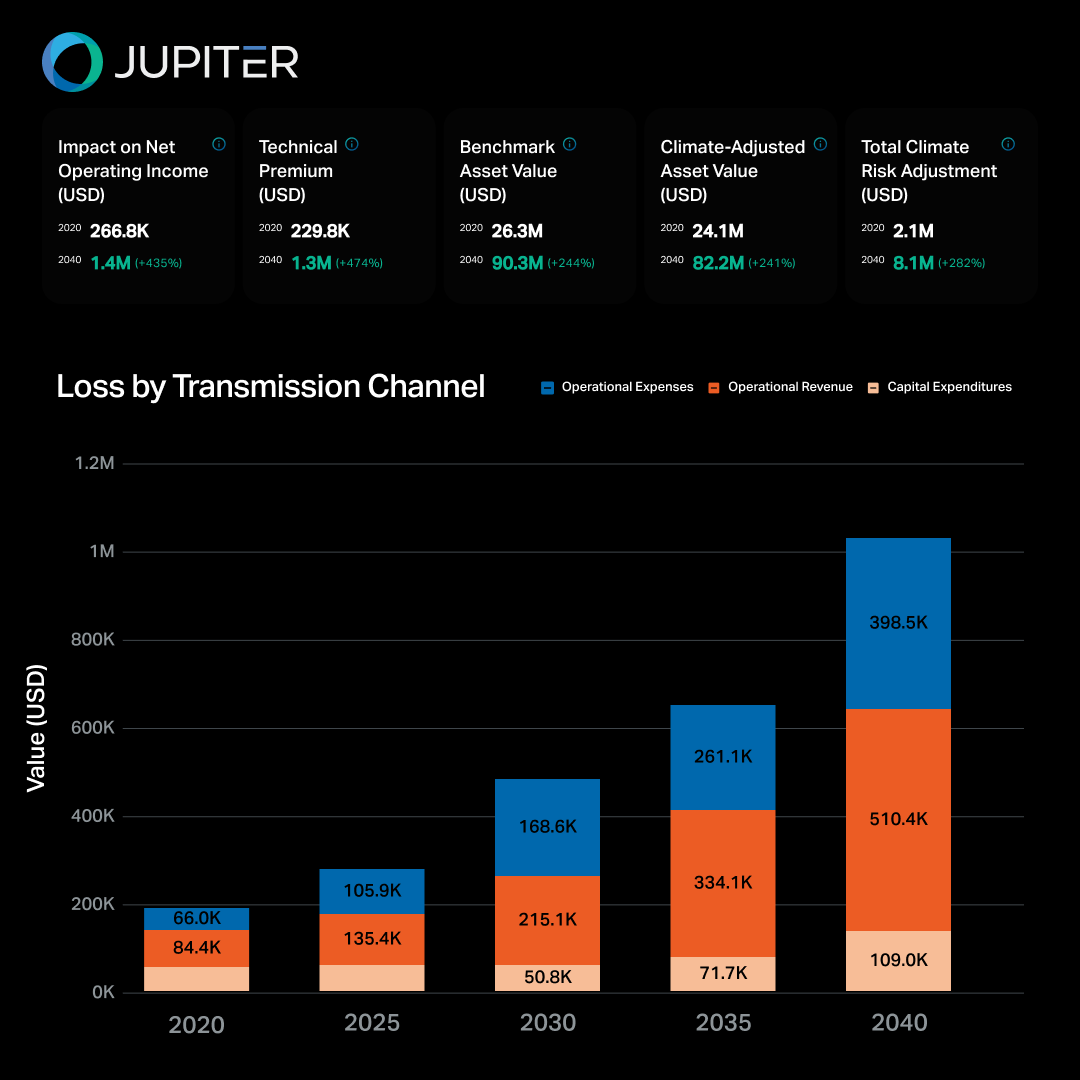

Annual flood-related downtime losses at this facility currently run $15.5K. By 2040, they reach $23.3K — a 50% increase. But the more consequential figure sits in the financial metrics layer. The impact on net operating income from all climate hazards, currently estimated at $266.8K annually, grows to $1.4M by 2040 — a 435% increase. The technical insurance premium rises by 474%, mostly due to the increasing flood risks. And the total climate risk adjustment — the gap between what this asset would be worth in a world without physical risk and what it is worth in the world as it is — stands at $2.1M today and reaches $12M by 2040, a 463% increase over twenty years.

That $12M figure is not a modeled abstraction. It is the present-day price of unmanaged physical risk, expressed in the financial language that lenders, investment committees, and asset managers use to make decisions. It is also precisely what GRESB's 2026 physical risk impact assessment indicators are asking reporters to produce — and what most group-level evidence frameworks cannot.

Compliance Is the Floor. Competitive Advantage Is the Ceiling.

There is a case for treating the 2026 standard updates as a compliance exercise. Complete the process, satisfy the validators, and protect the score.

But those who will benefit most from this cycle are the ones who recognize that GRESB's direction of travel mirrors what institutional capital markets are demanding independently.

Physical risk is already reshaping asset valuations, insurance pricing, and exit multiples. The pool of demonstrably climate-resilient real assets is finite and under increasing competitive pressure. Institutions that can identify, quantify, and act on physical risk at the asset level — with evidence that holds up under scrutiny — aren't just better GRESB reporters. They are better positioned at every stage of the investment lifecycle.

The 2026 standard update is a forcing function. Whether you use this floor to stand on or to build on is a strategic choice.

Your 2025 evidence won't pass 2026 validation. Here's the fix.

Every change described above — and the complete indicator-by-indicator blueprint for building evidence that satisfies the 2026 standard across all five assessments — is detailed in our new guide, The New Benchmark: What the GRESB Standard Actually Requires on Physical Climate Risk.

It covers every question type, every indicator code, and the specific evidence gap that tends to cost reporters the most points. If you're preparing to submit, this is the critical blueprint.

.png)