.webp)

.avif)

The U.S. housing market is an approximately $51.4 trillion cornerstone of economic stability. When stock markets tremble, a sound housing market can counteract the chaos, providing security in a volatile economy.

But climate-related risks like wildfire and wind pose serious threats to real estate assets. As natural disasters grow in frequency and severity, they may threaten current valuations and the broader financial systems that rely on a strong housing market.

While markets remain focused on inflation and interest rates, a more dangerous threat is quietly inflating beneath the surface. Jupiter Intelligence’s new research reveals a $389 billion climate bubble already embedded in the U.S. housing market, driven by decades of underpriced risk.

Jupiter’s latest report, The Climate Bubble, reveals an alarming reality: the U.S. housing market is currently on shaky ground. From the Sun Belt to the Midwest, millions of homes are exposed to alarming wind and wildfire risk. Yet these risks remain largely invisible in current insurance market data and home valuations.

Signs point to collapse

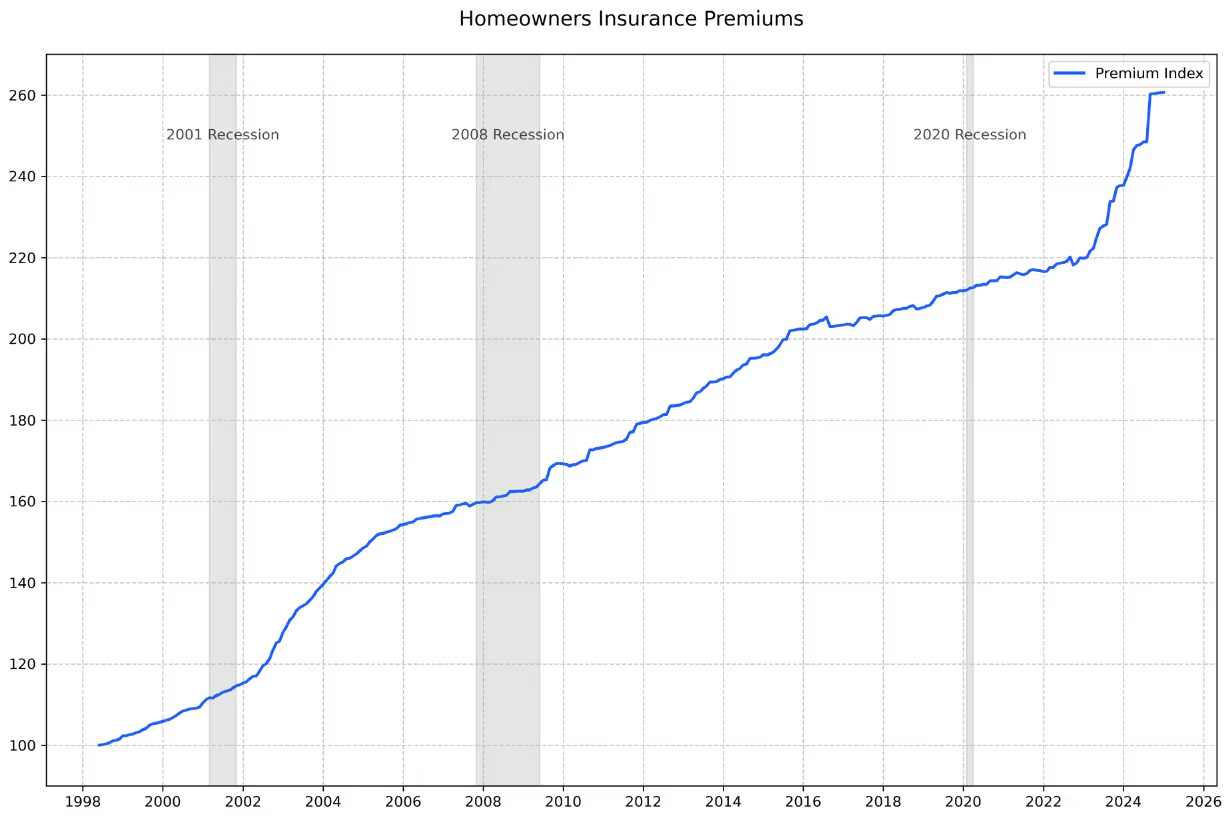

Insurance markets are flashing warning signs. Homeowners across the U.S. are facing a surge in insurance premiums, alongside a troubling rise in non-renewals, particularly in climate-vulnerable regions. This trend is more than a cost issue; it threatens the very mechanics of the housing market. Without insurance, mortgages can’t be issued. Without mortgages, home sales collapse. And when insurers exit, they take community stability with them, driving down property values and draining local tax bases.

Jupiter’s analysis shows that these rising premiums are not just a reflection of inflation or construction costs. In fact, even after adjusting for those conventional factors, there remains a 13% unexplained hike in insurance rates between 2022 and 2025.

Could climate be to blame?

Conducting one of the most comprehensive studies to date on the U.S. housing market, Jupiter studied single-family homes in the continental U.S., analyzing their current valuations and technical premiums to determine whether climate change is quietly interfering with insurance prices and home valuations.

True climate risk for the U.S. housing market is far higher than most people realize

Jupiter ran an analysis to determine whether current market price models are accurately estimating climate risk for the U.S. housing market. Our findings reveal that, while current market price models are accurately estimating risk for the vast majority of the market, premiums in very high-risk areas are nowhere near accurately priced.

In the 90th percentile of premiums, we see a clear divergence between what current models yield and where Jupiter’s forward-looking models place the true cost. In this top 10%, Jupiter’s forward-looking models reveal that current market premiums are nowhere near as high as they should be to account for the true risk of climate change.

“Part of the problem lies in how risk is assessed. Legacy catastrophe models rely on historical data and have repeatedly underestimated the true cost of disasters — by $71 billion in the case of Hurricane Katrina and $66 billion for Hurricane Harvey. Jupiter’s forward-looking climate models offer a more accurate lens, explaining 78.5% of current premium variation — versus far lower explanatory power from traditional methods.”

As insurance costs rise, home values fall

This divergence reveals a clear bubble in asset pricing. As insurance costs rise, home values eventually fall. Across the U.S., the total predicted loss in housing market value due to unpriced climate risk is astonishing: according to Jupiter’s analysis, the current U.S. housing market is overvalued by an estimated $389 billion.

Climate risk is concentrated in specific areas, creating ‘hot pockets’ where the impact is much greater. However, these hot pockets are not isolated to one region but are dispersed across the country.

Major hotspots include Southern California, Utah, Oregon, Wyoming, and Montana. In these areas, homeowners face steeper declines in property values as risks materialize. In high-risk areas, homes may carry up to $74,000 in unpriced climate risk. Jupiter’s data shows that for every $100 increase in climate-adjusted premiums, property values drop by an average of $1,000.

As these valuation bubbles burst, homeowners could see their equity erode, making it harder to refinance or sell properties. Financial institutions may face cascading impacts from declining collateral values and rising loan defaults. Given that their primary residence is the biggest driver of wealth for most Americans, a housing crisis would almost certainly result in a major financial crisis.

What does it mean for businesses?

This isn’t just a housing problem. With climate mispricing embedded in collateral valuations, loan books, and insurance portfolios, the ripple effects extend into financial markets, regulatory oversight, and global economic stability. For businesses and institutions, failing to quantify this exposure could translate into stranded assets and cascading losses.

In the past, soaring insurance premiums have signaled worse things to come. In what might be described as an economic domino effect, soaring insurance costs can cascade into loan defaults, collapsing collateral values, and, ultimately, significant financial instability.

If history tells us anything, it’s that mispriced assets ultimately lead to market corrections, even if the delay is significant. The economic shock that results may influence the global economy for years to come.

The best thing businesses can do to prepare is to rely on accurate, appropriate modelling to gauge the true climate risk exposure of their assets.